How Writing Goals In A 3x3 Grid Can Change Your Life

Set smarter goals with a simple 3x3 grid. Learn how career, personal, and life goals shape your future one step at a time.

We all know people who seem to stumble into success.

Maybe they got the right job, hit it big on an investment, or landed in the right place at the right time without planning.

That’s luck.

It happens, but it doesn’t happen often.

And when it does, it’s not the same as accomplishment—it’s just a circumstance.

The truth is, if we want to accomplish something meaningful, we need goals.

Without them, it’s like driving a car without a destination.

Sure, you can roll down the road, but where are you really going?

Think about simple things in life: going to the store, planning a meal, even setting your alarm.

Those are small goals, and they guide your actions more than you realize.

So why wouldn’t we do the same for the bigger things in life?

The 3x3 Grid That Keeps It Simple

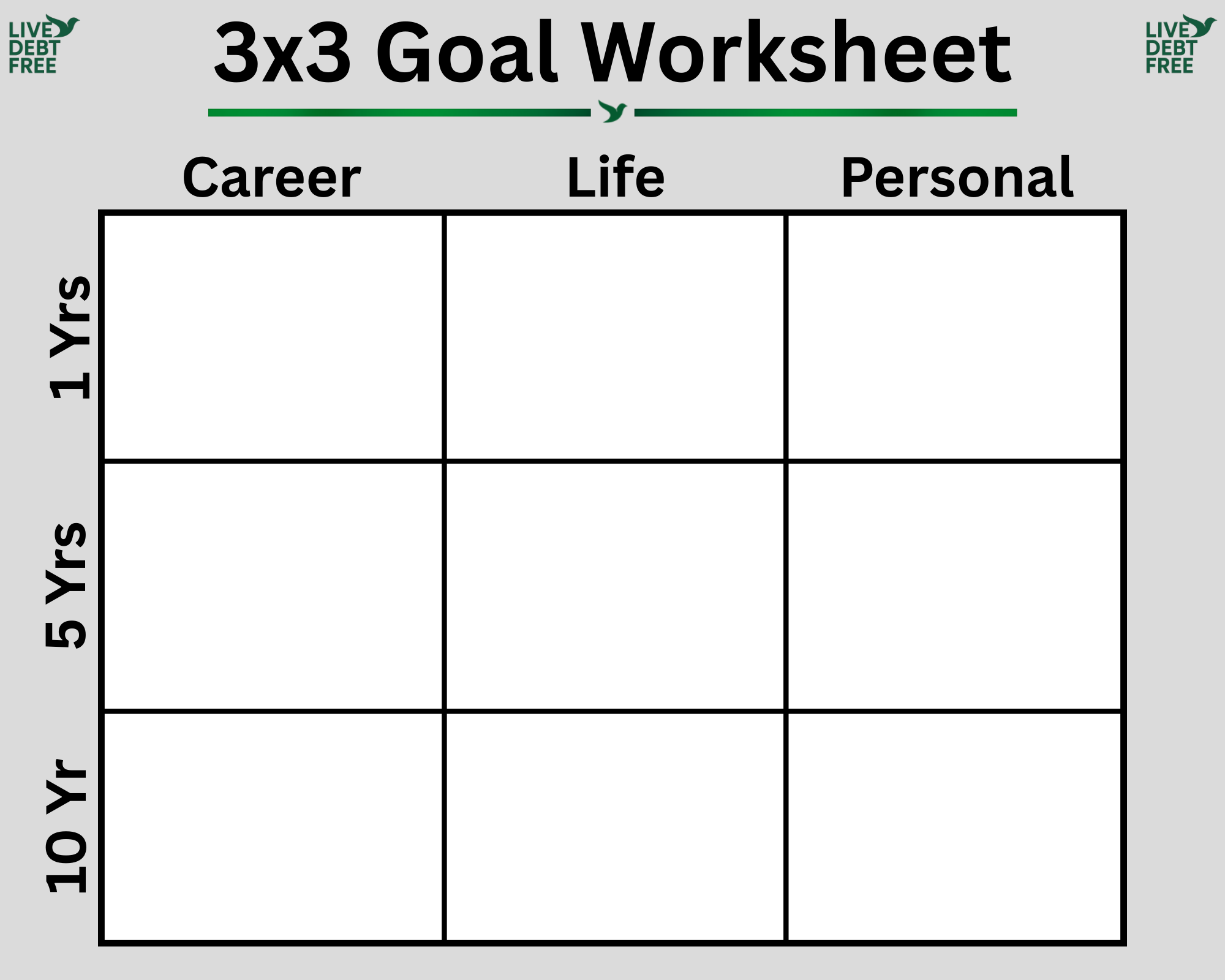

One of my mentors taught me a simple system for setting goals: a 3x3 grid.

Across the top, you write:

Career

Personal

Life

Down the side, you write:

1 Year

5 Years

10 Years

That’s it—nine boxes.

Nine chances to write down the goals that matter most to you.

In the top left, you’d write your 1-year career goal.

In the center, maybe your 5-year personal goal.

In the bottom right, your 10-year life goal.

Career, Personal, and Life Goals—What’s the Difference?

Career goals are straightforward: they’re about your job or business.

Maybe you want a promotion, a certification, or to start your own company.

Personal goals are more about you as a person.

Things like losing weight, becoming more confident, practicing positivity, or growing your faith.

Life goals affect what actually happens in your life: traveling the world, buying a house, retiring early, or learning a new skill you’ve always dreamed about.

Short, Mid, and Long Term

One-year goals are short term.

A year passes fast, but it’s enough time to get something done.

You can’t become a doctor in a year, but you could complete a certificate program.

If your goal is to lose 25 pounds in a year, that breaks down to about half a pound per week.

That’s realistic, safe, and doable.

Five-year goals are mid term.

This is where mastery comes into play.

You’ve probably heard that it takes about 10,000 hours to master something.

If you put in 40 hours a week, that’s just under five years.

That makes this time frame perfect for learning a skill deeply or reaching a major milestone that requires consistency.

Ten-year goals are long term.

These are about planning for the next phase of your life.

If you’re single, maybe that’s marriage or kids.

If you’re mid-career, maybe it’s retiring early or starting a business.

You don’t need to work on them daily, but they shape your daily choices.

For example, if you want to own a business in 10 years, you might start saving more today and cutting back on luxuries.

My Own Experience

I did this exercise back in 2017.

My 10-year life goal was simple: live debt free.

At the time, it felt impossible.

I had a mountain of debt hanging over me.

Fast forward, and I’m two years away from my 10-year deadline.

Today, I only have my mortgage left and I need to earn about $70k left to pay off.

I confident I can make it if I stay focused.

That grid, that piece of paper with nine boxes, has guided my decisions every single day since I wrote it down.

Why It Works

Goals don’t just give you something to aim for—they change the way you live.

When you know where you’re going, every choice matters.

Eating out less, skipping the new phone upgrade, saying no to unnecessary debt—all of those are little moves that line up with the bigger picture.

Final Thoughts

You don’t need to overcomplicate goal setting.

A simple 3x3 grid can be life-changing if you actually use it.

Write your goals down.

Keep them realistic.

Check them often.

Then let them guide your daily choices.

That’s how you break free—one dollar, one step, one goal at a time.

Disclaimer: The content on Live Debt Free is for educational and informational purposes only and should not be considered financial advice. Always consult with a qualified financial advisor before making decisions regarding your personal finances. We are not responsible for any outcomes resulting from the use of the information provided.